UNITED STATES

SECURITIES AND EXCHANGE COMMISSION

Washington, D.C. 20549

FORM 10-K

|

☒ |

ANNUAL REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

For the fiscal year ended December 31, 2020

OR

|

☐ |

TRANSITION REPORT PURSUANT TO SECTION 13 OR 15(d) OF THE SECURITIES EXCHANGE ACT OF 1934 |

Commission File Number 814-01190

OWL ROCK CAPITAL CORPORATION

(Exact name of Registrant as specified in its Charter)

|

Maryland |

|

47-5402460 |

|

(State or other jurisdiction of incorporation or organization) |

|

(I.R.S. Employer Identification No.) |

|

|

|

|

|

399 Park Avenue, 38th Floor, New York, New York |

|

10022 |

|

(Address of principal executive offices) |

|

(Zip Code) |

Registrant’s telephone number, including area code: (212) 419-3000

Securities registered pursuant to Section 12(b) of the Act:

|

Title of each class |

Trading Symbol(s) |

Name of each exchange on which registered |

|

Common Stock, $0.01 par value per share |

ORCC |

The New York Stock Exchange |

Securities registered pursuant to Section 12(g) of the Act:

None

Indicate by check mark if the Registrant is a well-known seasoned issuer, as defined in Rule 405 of the Securities Act. YES ☒ NO ☐

Indicate by check mark if the Registrant is not required to file reports pursuant to Section 13 or 15(d) of the Act. YES ☐ NO ☒

Indicate by check mark whether the Registrant: (1) has filed all reports required to be filed by Section 13 or 15(d) of the Securities Exchange Act of 1934 during the preceding 12 months (or for such shorter period that the Registrant was required to file such reports), and (2) has been subject to such filing requirements for the past 90 days. YES ☒ NO ☐

Indicate by check mark whether the Registrant has submitted every Interactive Data File required to be submitted pursuant to Rule 405 of Regulation S-T (§232.405 of this chapter) during the preceding 12 months (or for such shorter period that the Registrant was required to submit such files). YES ☐ NO ☐

Indicate by check mark whether the Registrant is a large accelerated filer, an accelerated filer, a non-accelerated filer, a smaller reporting company, or an emerging growth company. See the definition of “large accelerated filer”, “accelerated filer”, “smaller reporting company” and “emerging growth company” in Rule 12b-2 of the Exchange Act.

|

Large accelerated filer |

☒ |

|

Accelerated filer |

☐ |

|

|

|

|

|

|

|

Non-accelerated filer |

☐ |

|

Small reporting company |

☐ |

|

|

|

|

|

|

|

Emerging growth company |

☐ |

|

|

|

If an emerging growth company, indicate by check mark if the registrant has elected not to use the extended transition period for complying with any new or revised financial accounting standards provided pursuant to Section 13(a) of the Exchange Act. ☐

Indicate by check mark whether the registrant has filed a report on and attestation to its management’s assessment of the effectiveness of its internal control over financial reporting under Section 404(b) of the Sarbanes-Oxley Act (15 U.S.C. 7262(b)) by the registered public accounting firm that prepared or issued its audit report. ☒

Indicate by check mark whether the Registrant is a shell company (as defined in Rule 12b-2 of the Exchange Act). YES ☐ NO ☒

The aggregate market value of the common stock held by non-affiliates of the registrant on June 30, 2020 based on the closing price on that date of $12.33 on The New York Stock Exchange, was approximately $4,649,632,483.

The number of shares of the registrant’s common stock $0.01 par value per share, outstanding at February 23, 2021 was 391,401,787.

i

Table of Contents

|

|

|

|

|

Page |

|

PART I |

|

|

|

|

|

Item 1. |

|

|

2 |

|

|

Item 1A. |

|

|

32 |

|

|

Item 1B. |

|

|

68 |

|

|

Item 2. |

|

|

68 |

|

|

Item 3. |

|

|

68 |

|

|

Item 4. |

|

|

68 |

|

|

|

|

|

|

|

|

PART II |

|

|

|

|

|

Item 5. |

|

|

69 |

|

|

Item 6. |

|

|

79 |

|

|

Item 7. |

|

Management’s Discussion and Analysis of Financial Condition and Results of Operations |

|

82 |

|

Item 7A. |

|

|

149 |

|

|

Item 8. |

|

|

F-1 |

|

|

Item 9. |

|

Changes in and Disagreements with Accountants on Accounting and Financial Disclosure |

|

150 |

|

Item 9A. |

|

|

150 |

|

|

Item 9B. |

|

|

150 |

|

|

|

|

|

|

|

|

PART III |

|

|

|

|

|

Item 10. |

|

|

150 |

|

|

Item 11. |

|

|

162 |

|

|

Item 12. |

|

Security Ownership of Certain Beneficial Owners and Management and Related Shareholder Matters |

|

163 |

|

Item 13. |

|

Certain Relationships and Related Transactions, and Director Independence |

|

164 |

|

Item 14. |

|

|

166 |

|

|

|

|

|

|

|

|

PART IV |

|

|

|

|

|

Item 15. |

|

|

167 |

|

|

Item 16. |

|

|

174 |

|

|

|

|

|

175 |

ii

CAUTIONARY STATEMENT REGARDING FORWARD-LOOKING STATEMENTS

This report contains forward-looking statements that involve substantial risks and uncertainties. Such statements involve known and unknown risks, uncertainties and other factors and undue reliance should not be placed thereon. These forward-looking statements are not historical facts, but rather are based on current expectations, estimates and projections about Owl Rock Capital Corporation (the “Company,” “we” or “our”), our current and prospective portfolio investments, our industry, our beliefs and opinions, and our assumptions. Words such as “anticipates,” “expects,” “intends,” “plans,” “will,” “may,” “continue,” “believes,” “seeks,” “estimates,” “would,” “could,” “should,” “targets,” “projects,” “outlook,” “potential,” “predicts” and variations of these words and similar expressions are intended to identify forward-looking statements. These statements are not guarantees of future performance and are subject to risks, uncertainties and other factors, some of which are beyond our control and difficult to predict and could cause actual results to differ materially from those expressed or forecasted in the forward-looking statements, including without limitation:

|

|

• |

an economic downturn could impair our portfolio companies’ ability to continue to operate, which could lead to the loss of some or all of our investments in such portfolio companies; |

|

|

• |

an economic downturn could disproportionately impact the companies that we intend to target for investment, potentially causing us to experience a decrease in investment opportunities and diminished demand for capital from these companies; |

|

|

• |

an economic downturn could also impact availability and pricing of our financing and our ability to access the debt and equity capital markets; |

|

|

• |

a contraction of available credit and/or an inability to access the equity markets could impair our lending and investment activities; |

|

|

• |

the impact of the novel strain of coronavirus known as “COVID-19” and related changes in base interest rates and significant market volatility on our business, our portfolio companies, our industry and the global economy; |

|

|

• |

interest rate volatility, including the decommissioning of LIBOR, could adversely affect our results, particularly if we elect to use leverage as part of our investment strategy; |

|

|

• |

currency fluctuations could adversely affect the results of our investments in foreign companies, particularly to the extent that we receive payments denominated in foreign currency rather than U.S. dollars; |

|

|

• |

our future operating results; |

|

|

• |

our business prospects and the prospects of our portfolio companies including our and their ability to achieve our respective objectives as a result of the current COVID-19 pandemic; |

|

|

• |

our contractual arrangements and relationships with third parties; |

|

|

• |

the ability of our portfolio companies to achieve their objectives; |

|

|

• |

competition with other entities and our affiliates for investment opportunities; |

|

|

• |

the speculative and illiquid nature of our investments; |

|

|

• |

the use of borrowed money to finance a portion of our investments as well as any estimates regarding potential use of leverage; |

|

|

• |

the adequacy of our financing sources and working capital; |

|

|

• |

the loss of key personnel; |

|

|

• |

the timing of cash flows, if any, from the operations of our portfolio companies; |

|

|

• |

the ability of Owl Rock Capital Advisors LLC (“the Adviser” or “our Adviser”) to locate suitable investments for us and to monitor and administer our investments; |

|

|

• |

the ability of the Adviser to attract and retain highly talented professionals; |

|

|

• |

our ability to qualify for and maintain our tax treatment as a regulated investment company (“RIC”) under Subchapter M of the Internal Revenue Code of 1986, as amended (the “Code”), and as a business development company (“BDC”); |

|

|

• |

the effect of legal, tax and regulatory changes; and |

|

|

• |

other risks, uncertainties and other factors previously identified in the reports and other documents we have filed with the Securities and Exchange Commission (“SEC”). |

Although we believe that the assumptions on which these forward-looking statements are based are reasonable, any of those assumptions could prove to be inaccurate, and as a result, the forward-looking statements based on those assumptions also could be inaccurate. In light of these and other uncertainties, the inclusion of a projection or forward-looking statement in this report should not be regarded as a representation by us that our plans and objectives will be achieved. These forward-looking statements apply only as of the date of this report. Moreover, we assume no duty and do not undertake to update the forward-looking statements. Because we are an investment company, the forward-looking statements and projections contained in this report are excluded from the safe harbor protection provided by Section 21E of the U.S. Securities Exchange Act of 1934, as amended (the “Exchange Act”).

1

Our Company

Owl Rock Capital Corporation was formed on October 15, 2015 as a corporation under the laws of the State of Maryland. We are a specialty finance company focused on lending to U.S. middle-market companies. Since we began investment activities in April 2016 through December 31, 2020, our Adviser and its affiliates have originated $27.7 billion aggregate principal amount of investments, of which $25.8 billion of aggregate principal amount of investments prior to any subsequent exits or repayments, was retained by either us or a fund advised by our Adviser or its affiliates. Our capital will be used by our portfolio companies to support growth, acquisitions, market or product expansion, refinancings and/or recapitalizations.

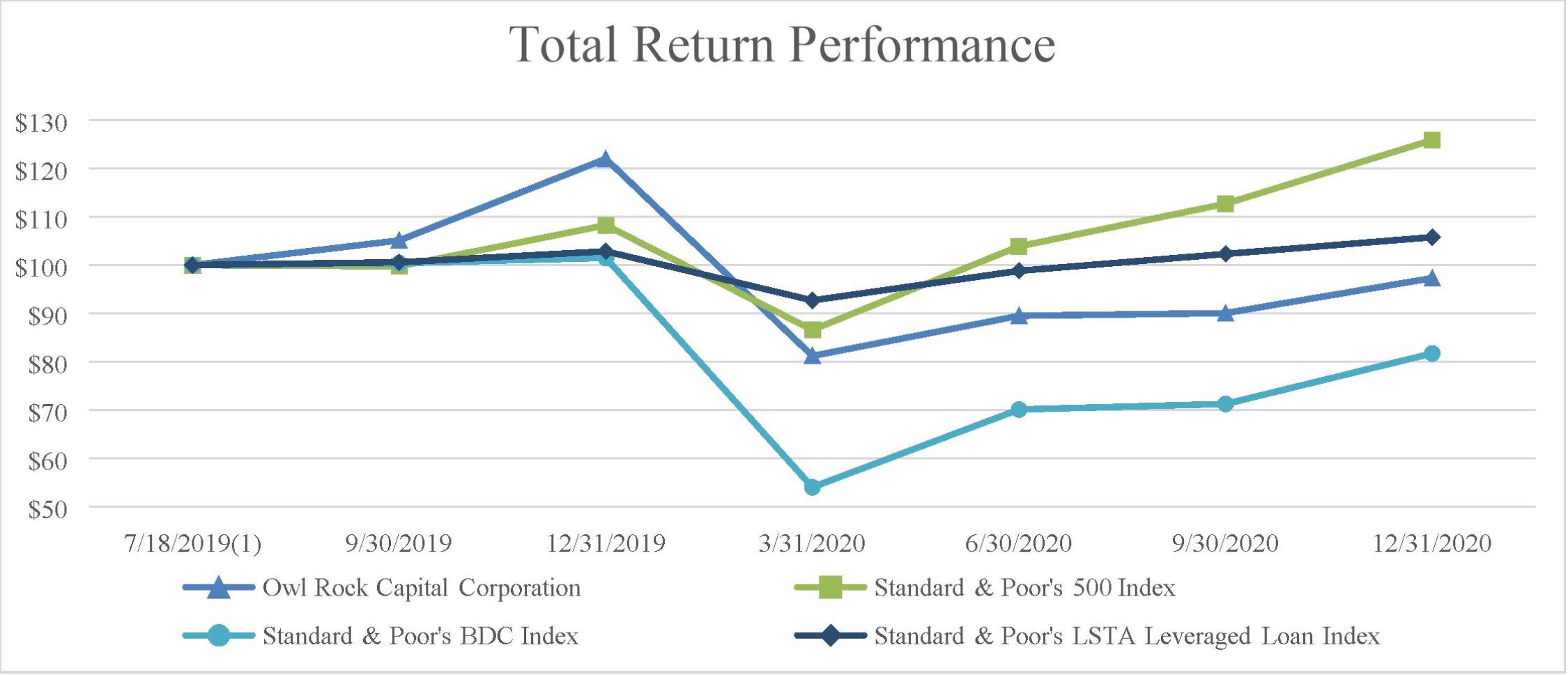

On July 22, 2019, we closed our initial public offering (“IPO”), issuing 10 million shares of our common stock at a public offering price of $15.30 per share, and on August 2, 2019, the underwriters exercised their option to purchase an additional 1.5 million shares of our common stock at a purchase price of $15.30 per share. Net of underwriting fees and offering costs, we received total cash proceeds of $164.0 million. Our common stock began trading on the New York Stock Exchange (“NYSE”) under the symbol “ORCC” on July 18, 2019.

We define “middle market companies” to generally mean companies with earnings before interest expense, income tax expense, depreciation and amortization (“EBITDA”) between $10 million and $250 million annually, and/or annual revenue of $50 million to $2.5 billion at the time of investment. We may on occasion invest in smaller or larger companies if an attractive opportunity presents itself, especially when there are dislocations in the capital markets, including the high yield and syndicated loan markets. Our target credit investments will typically have maturities between three and ten years and generally range in size between $20 million and $250 million. The investment size will vary with the size of our capital base. As of December 31, 2020, excluding certain investments that fall outside of our typical borrower profile, our portfolio companies representing 93.8% of our total debt portfolio based on fair value, had weighted average annual revenue of $460 million and weighted average annual EBITDA of $100 million.

We invest in senior secured or unsecured loans, subordinated loans or mezzanine loans and, to a lesser extent, equity and equity-related securities including warrants, preferred stock and similar forms of senior equity, which may or may not be convertible into a portfolio company’s common equity. Our investment objective is to generate current income and, to a lesser extent, capital appreciation by targeting investment opportunities with favorable risk-adjusted returns. While we believe that current market conditions favor extending credit to middle market companies in the United States, our investment strategy is intended to generate favorable returns across credit cycles with an emphasis on preserving capital. As of December 31, 2020, based on fair value, our portfolio consisted of 77.5% first lien debt investments, 18.5% second-lien debt investments, 0.5% unsecured debt investments, 1.0% investment funds and vehicles and 2.5% equity investments. As of December 31, 2020, 99.9% of our debt investments based on fair value are floating rate in nature and subject to interest rate floors. As of December 31, 2020 we had investments in 119 portfolio companies, with an average investment size in each of our portfolio companies of approximately $91.1 million based on fair value.

As of December 31, 2020, our portfolio was invested across 29 different industries. The largest industry in our portfolio as of December 31, 2020 was internet software and services, which represented, as a percentage of our portfolio, 11.1%, based on fair value.

We are an externally managed, closed-end management investment company that has elected to be regulated as a BDC under the Investment Company Act of 1940 Act, as amended (the “1940 Act”). We have elected to be treated, and intend to qualify annually, as a RIC under the Code for U.S. federal income tax purposes. As a BDC and a RIC, we are required to comply with certain regulatory requirements. As a BDC, at least 70% of our assets must be assets of the type listed in Section 55(a) of the 1940 Act, as described herein. We will not invest more than 20% of our total assets in companies whose principal place of business is outside the United States. See “— Regulation as a Business Development Company” and “— Certain U.S. Federal Income Tax Considerations.”

We generally intend to distribute, out of assets legally available for distribution, substantially all of our available earnings, on a quarterly basis, as determined by our Board of Directors (the “Board”) in its sole discretion.

Certain consolidated subsidiaries of ours are subject to U.S. federal and state corporate-level income taxes.

To achieve our investment objective, we will leverage the Adviser’s investment team’s extensive network of relationships with other sophisticated institutions to source, evaluate and, as appropriate, partner with on transactions. There are no assurances that we will achieve our investment objective.

We may borrow money from time to time if immediately after such borrowing, the ratio of our total assets (less total liabilities other than indebtedness represented by senior securities) to our total indebtedness represented by senior securities plus preferred stock, if any, is at 150%. This means that generally, we can borrow up to $2 for every $1 of investor equity.

2

We currently have in place a senior secured revolving credit facility (the “Revolving Credit Facility”) and three special purpose vehicle asset credit facilities (the “SPV Asset Facility II,” the “SPV Asset Facility III,” and the “SPV Asset Facility IV,” respectively), and in the future may enter into additional credit facilities. In addition, we have issued unsecured notes maturing in 2023 (the “2023 Notes”) in a private placement and unsecured notes maturing in 2024, 2025 and 2026 (the “2024 Notes,” the “2025 Notes,” the “July 2025 Notes,” the “2026 Notes” and the “July 2026 Notes,” respectively) in registered offerings and in the future may issue additional unsecured notes. The special purpose vehicle asset credit facilities are a financing facilities pursuant to which we formed a wholly owned subsidiary, or SPV, which enters into a credit agreement. We periodically sell and contribute investments to the SPV and the SPV uses the proceeds from the credit agreement to finance the purchase of assets, including from us. We have also entered into five term debt securitization transactions, also known as collateralized loan obligation transactions (“CLO I,” “CLO II,” “CLO III,” “CLO IV” and “CLO V,” respectively) and in the future may enter into additional collateralized loan obligation transactions. We expect to use our credit facilities and other borrowings, along with proceeds from the rotation of our portfolio, to finance our investment objectives. See “— Regulation as a Business Development Company” for discussion of BDC regulation and other regulatory considerations. See “ITEM 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS — Debt.”

The Adviser and Administrator – Owl Rock Capital Advisors LLC

Owl Rock Capital Advisors LLC serves as our investment adviser pursuant to an investment advisory agreement between us and the Adviser, which was originally entered into on March 1, 2016 (the “Original Investment Advisory Agreement”) and which, with the approval of the Board, including a majority of our independent directors, was amended and restated on February 27, 2019 (as amended and restated, the “First Amended and Restated Investment Advisory Agreement”) to reduce the fees that the Company will pay the Adviser following an Exchange Listing, which occurred on July 18, 2019, and which was further amended and restated on March 31, 2020 to reduce the management fee payable to the Adviser when the Company's asset coverage ratio calculated in accordance with Sections 18 and 61 of the 1940 Act is below 200% (as amended and restated, the "Investment Advisory Agreement"). See “Investment Advisory Agreement” below. The Adviser also serves as our Administrator pursuant to an Administration Agreement between us and the Adviser which was entered into on March 1, 2016 (the “Administration Agreement”). See “Administration Agreement” below. The Adviser is registered with the SEC as an investment adviser under the Investment Advisers Act of 1940, as amended (the “Advisers Act”). The Adviser is an indirect subsidiary of Owl Rock Capital Partners LP (“Owl Rock Capital Partners”). Owl Rock Capital Partners is led by its three co-founders, Douglas I. Ostrover, Marc S. Lipschultz and Craig W. Packer. The Adviser’s investment team (the “Investment Team”) is also led by Douglas I. Ostrover, Marc S. Lipschultz and Craig W. Packer and is supported by certain members of the Adviser’s senior executive team and the investment committee (the “Investment Committee”). The Investment Committee is comprised of Douglas I. Ostrover, Marc S. Lipschultz, Craig W. Packer and Alexis Maged. Subject to the overall supervision of the Board, the Adviser manages our day-to-day operations, and provides investment advisory and management services to us.

On December 23, 2020, Owl Rock Capital Group, LLC (“Owl Rock Capital Group”), the parent of the Adviser (and a subsidiary of Owl Rock Capital Partners), and Dyal Capital Partners (“Dyal”) announced they are merging to form Blue Owl Capital Inc. (“Blue Owl”). Blue Owl will enter the public market via its acquisition by Altimar Acquisition Corporation (NYSE:ATAC) (“Altimar”), a special purpose acquisition company (the “Transaction”). If the Transaction is consummated, there will be no changes to the Company’s investment strategy or the Adviser’s investment team or investment process with respect to the Company; however, the Transaction will result in a change in control of the Adviser, which will be deemed an assignment of the Investment Advisory Agreement in accordance with the 1940 Act. As a result, the Board, after considering the Transaction and subsequent change in control, has determined that upon consummation of the Transaction and subject to the approval of the Company’s shareholders at a special meeting expected to be held on March 17, 2021, the Company should enter into a third amended and restated investment advisory agreement with the Adviser on terms that are identical to the Investment Advisory Agreement. The Board also determined that upon consummation of the Transaction, the Company should enter into an amended and restated administration agreement with the Adviser on terms that are identical to the Administration Agreement.

The Adviser is affiliated with Owl Rock Technology Advisors LLC (“ORTA”), Owl Rock Private Fund Advisors LLC (“ORPFA”) and Owl Rock Diversified Advisors LLC (“ORDA” and together with the Adviser, ORTA and ORPFA, the “Owl Rock Advisors”). As of December 31, 2020, the Owl Rock Advisors managed $27.1 billion in AUM. The Owl Rock Advisors focus on direct lending to middle market companies primarily in the United States under the following four investment strategies:

3

|

Strategy |

Funds |

Asset Under Management |

| Diversified Lending. The Owl Rock Advisors primarily originate and make loans to, and make debt and equity investments in, U.S. middle market companies The Owl Rock Advisors invest in senior secured or unsecured loans, subordinated loans or mezzanine loans and, to a lesser extent, equity and equity-related securities including warrants, preferred stock and similar forms of senior equity, which may or may not be convertible into a portfolio company’s common equity. The investment objective of the funds with this investment strategy is to generate current income and, to a lesser extent, capital appreciation by targeting investment opportunities with favorable risk-adjusted returns.

|

The diversified lending strategy is currently managed through four BDCs: the Company, Owl Rock Capital Corporation II (“ORCC II”), Owl Rock Capital Corporation III (“ORCC III”) and Owl Rock Core Income Corp. (“ORCIC”). |

As of December 31, 2020, the Owl Rock Advisors have $17.0 billion of assets under management across these products. |

|

Technology Lending. The Owl Rock Advisors are focused primarily on originating and making debt and equity investments in technology-related companies based primarily in the United States. The Owl Rock Advisors originate and invest in senior secured or unsecured loans, subordinated loans or mezzanine loans, and equity-related securities including common equity, warrants, preferred stock and similar forms of senior equity, which may or may not be convertible into a portfolio company’s common equity. The investment objective of the funds with this investment strategy is to maximize total return by generating current income from debt investments and other income producing securities, and capital appreciation from our equity and equity-linked investments. |

The technology lending strategy is managed through Owl Rock Technology Finance Corp. (“ORTF” and together with the Company, ORCC II, ORCC III and ORCIC, the “Owl Rock BDCs”), a BDC. |

As of December 31, 2020, the Owl Rock Advisors have $5.4 billion of assets under management across these products. |

|

First Lien Lending. The Owl Rock Advisers seek to realize significant current income with an emphasis on preservation of capital primarily through originating primary transactions in and, to a lesser extent, secondary transactions of first lien senior secured loans in or related to middle market businesses based primarily in the United States. |

The first lien lending strategy is managed through private funds and separately managed accounts (the “First Lien Funds”). |

As of December 31, 2020, the Owl Rock Advisors have $3.0 billion of assets under management across these products. |

|

Opportunistic Lending. The Owl Rock Advisors intend to make opportunistic investments in U.S. middle-market companies by providing a variety of approaches to financing, including but not limited to originating and/or investing in secured debt, unsecured debt, mezzanine debt, other subordinated debt, interests senior to common equity, as well as equity securities (or rights to acquire equity securities) which may or may not be acquired in connection with a debt financing transaction, and doing any and all things necessary, convenient or incidental thereto as necessary or desirable to promote and carry out such purpose. The funds with this investment strategy seek to generate attractive risk-adjusted returns by taking advantage of credit opportunities in U.S. middle-market companies with liquidity needs and market leaders seeking to improve their balance sheets. |

The opportunistic lending strategy is managed through a private fund and separately managed accounts (the “Opportunistic Lending Funds” and together with the First Lien Funds, the “Owl Rock Private Funds”). |

As of December 31, 2020, the Owl Rock Advisors have $1.7 billion of assets under management across these products. |

We refer to the Owl Rock BDCs and the Owl Rock Private Funds, as the “Owl Rock Clients.”

The Owl Rock Advisers may provide management or investment advisory services to entities that have overlapping objectives with us. The Adviser and its affiliates may face conflicts in the allocation of investment opportunities to us and others. In order to address these conflicts, the Owl Rock Advisers have put in place an allocation policy that addresses the allocation of investment opportunities as well as co-investment restrictions under the 1940 Act.

4

In addition, we, the Adviser and certain of its affiliates have been granted exemptive relief by the SEC to co-invest with other funds managed by the Adviser or its affiliates in a manner consistent with our investment objective, positions, policies, strategies and restrictions as well as regulatory requirements and other pertinent factors. Pursuant to such exemptive relief, we generally are permitted to co-invest with certain of our affiliates if a “required majority” (as defined in Section 57(o) of the 1940 Act) of our independent directors make certain conclusions in connection with a co-investment transaction, including that (1) the terms of the transaction, including the consideration to be paid, are reasonable and fair to us and our shareholders and do not involve overreaching of us or our shareholders on the part of any person concerned, (2) the transaction is consistent with the interests of our shareholders and is consistent with our investment objective and strategies, and (3) the investment by our affiliates would not disadvantage us, and our participation would not be on a basis different from or less advantageous than that on which our affiliates are investing. In addition, pursuant to an exemptive order issued by the SEC on April 8, 2020 and applicable to all BDCs, through December 31, 2020, we were permitted, subject to the satisfaction of certain conditions, to complete follow-on investments in our existing portfolio companies with certain other funds managed by the Adviser or its affiliates and covered by our exemptive relief, even if such private funds had not previously invested in such existing portfolio company. Without this order, private funds would generally not be able to participate in such follow-on investments with us unless the private funds had previously acquired securities of the portfolio company in a co-investment transaction with us. Although the conditional exemptive order has expired, the SEC’s Division of Investment Management has indicated that until March 31, 2021, it will not recommend enforcement action, to the extent that any BDC with an existing coinvestment order continues to engage in certain transactions described in the conditional exemptive order, pursuant to the same terms and conditions described therein. The Owl Rock Advisers’ allocation policy incorporates the conditions of the exemptive relief. As a result of the exemptive relief, there could be significant overlap in our investment portfolio and the investment portfolio of the Owl Rock Clients and/or other funds established by the Owl Rock Advisers that could avail themselves of the exemptive relief. See “Item 1A. Risk Factors —Risks Related to our Adviser and its Affiliates — We may compete for capital and investment opportunities with other entities managed by our Adviser or its affiliates, subjecting our Adviser to certain conflicts of interest.

The Adviser or its affiliates may engage in certain origination activities and receive attendant arrangement, structuring or similar fees. See “Item 1A. Risk Factors —Risks Related to our Adviser and its Affiliates — The Adviser and its affiliates may face conflicts of interest with respect to services performed for issuers in which we invest.”

The Adviser’s address is 399 Park Avenue, 38th floor, New York, NY 10022.

We believe the middle-market lending environment provides opportunities for us to meet our goal of making investments that generate attractive risk-adjusted returns based on a combination of the following factors, which continue to remain true in the current environment, with the economic shutdown resulting from the COVID-19 national health emergency:

Limited Availability of Capital for Middle-Market Companies. We believe that regulatory and structural changes in the market have reduced the amount of capital available to U.S. middle-market companies. In particular, we believe there are currently fewer providers of capital to middle market companies. We believe that many commercial and investment banks have, in recent years, de-emphasized their service and product offerings to middle-market businesses in favor of lending to large corporate clients and managing capital markets transactions. In addition, these lenders may be constrained in their ability to underwrite and hold bank loans and high yield securities for middle-market issuers as they seek to meet existing and future regulatory capital requirements. We also believe that there is a lack of market participants that are willing to hold meaningful amounts of certain middle-market loans. As a result, we believe our ability to minimize syndication risk for a company seeking financing by being able to hold its loans without having to syndicate them, coupled with reduced capacity of traditional lenders to serve the middle-market, present an attractive opportunity to invest in middle-market companies.

Capital Markets Have Been Unable to Fill the Void in U.S. Middle Market Finance Left by Banks. While underwritten bond and syndicated loan markets have been robust in recent years, middle market companies are less able to access these markets for reasons including the following:

High-Yield Market – Middle market companies generally are not issuing debt in an amount large enough to be an attractively sized bond. High yield bonds are generally purchased by institutional investors who, among other things, are focused on the liquidity characteristics of the bond being issued. For example, mutual funds and exchange traded funds (“ETFs”) are significant buyers of underwritten bonds. However, mutual funds and ETFs generally require the ability to liquidate their investments quickly in order to fund investor redemptions and/or comply with regulatory requirements. Accordingly, the existence of an active secondary market for bonds is an important consideration in these entities’ initial investment decision. Because there is typically little or no active secondary market for the debt of U.S. middle market companies, mutual funds and ETFs generally do not provide debt capital to U.S. middle market companies. We believe this is likely to be a persistent problem and creates an advantage for those like us who have a more stable capital base and have the ability to invest in illiquid assets.

5

Syndicated Loan Market – While the syndicated loan market is modestly more accommodating to middle market issuers, as with bonds, loan issue size and liquidity are key drivers of institutional appetite and, correspondingly, underwriters’ willingness to underwrite the loans. Loans arranged through a bank are done either on a “best efforts” basis or are underwritten with terms plus provisions that permit the underwriters to change certain terms, including pricing, structure, yield and tenor, otherwise known as “flex”, to successfully syndicate the loan, in the event the terms initially marketed are insufficiently attractive to investors. Furthermore, banks are generally reluctant to underwrite middle market loans because the arrangement fees they may earn on the placement of the debt generally are not sufficient to meet the banks’ return hurdles. Loans provided by companies such as ours provide certainty to issuers in that we can commit to a given amount of debt on specific terms, at stated coupons and with agreed upon fees. As we are the ultimate holder of the loans, we do not require market “flex” or other arrangements that banks may require when acting on an agency basis.

Robust Demand for Debt Capital. We believe U.S. middle market companies will continue to require access to debt capital to refinance existing debt, support growth and finance acquisitions. In addition, we believe the large amount of uninvested capital held by funds of private equity firms, estimated by Preqin Ltd., an alternative assets industry data and research company, to be $1.5 trillion as of October 2020 will continue to drive deal activity. We expect that private equity sponsors will continue to pursue acquisitions and leverage their equity investments with secured loans provided by companies such as us.

The Middle Market is a Large Addressable Market. According to GE Capital’s National Center for the Middle Market 4th quarter 2020 Middle Market Indicator, there are approximately 200,000 U.S. middle market companies, which have approximately 48 million aggregate employees. Moreover, the U.S. middle market accounts for one-third of private sector gross domestic product (“GDP”). GE defines U.S. middle market companies as those between $10 million and $1 billion in annual revenue, which we believe has significant overlap with our definition of U.S. middle market companies.

Attractive Investment Dynamics. An imbalance between the supply of, and demand for, middle market debt capital creates attractive pricing dynamics. We believe the directly negotiated nature of middle market financings also generally provides more favorable terms to the lender, including stronger covenant and reporting packages, better call protection, and lender-protective change of control provisions. Additionally, we believe BDC managers’ expertise in credit selection and ability to manage through credit cycles has generally resulted in BDCs experiencing lower loss rates than U.S. commercial banks through credit cycles. Further, we believe that historical middle market default rates have been lower, and recovery rates have been higher, as compared to the larger market capitalization, broadly distributed market, leading to lower cumulative losses. Lastly, we believe that in the current environment, as the economy reopens following the economic shutdown resulting from the COVID-19 national health emergency, lenders with available capital may be able to take advantage of attractive investment opportunities as the economy reopens and may be able to achieve improved economic spreads and documentation terms.

Conservative Capital Structures. Following the credit crisis, which we define broadly as occurring between mid-2007 and mid-2009, lenders have generally required borrowers to maintain more equity as a percentage of their total capitalization, specifically to protect lenders during economic downturns. With more conservative capital structures, U.S. middle market companies have exhibited higher levels of cash flows available to service their debt. In addition, U.S. middle market companies often are characterized by simpler capital structures than larger borrowers, which facilitates a streamlined underwriting process and, when necessary, restructuring process.

Attractive Opportunities in Investments in Loans. We invest in senior secured or unsecured loans, subordinated loans or mezzanine loans and, to a lesser extent, equity and equity-related securities. We believe that opportunities in senior secured loans are significant because of the floating rate structure of most senior secured debt issuances and because of the strong defensive characteristics of these types of investments. Given the current low interest rate environment, we believe that debt issues with floating interest rates offer a superior return profile as compared with fixed-rate investments, since floating rate structures are generally less susceptible to declines in value experienced by fixed-rate securities in a rising interest rate environment. Senior secured debt also provides strong defensive characteristics. Senior secured debt has priority in payment among an issuer’s security holders whereby holders are due to receive payment before junior creditors and equity holders. Further, these investments are secured by the issuer’s assets, which may provide protection in the event of a default.

Potential Competitive Advantages

We believe that the Adviser’s disciplined approach to origination, fundamental credit analysis, portfolio construction and risk management should allow us to achieve attractive risk-adjusted returns while preserving our capital. We believe that we represent an attractive investment opportunity for the following reasons:

Experienced Team with Expertise Across all Levels of the Corporate Capital Structure. The members of the Investment Committee have over 25 years of experience in private lending and investing at all levels of a company’s capital structure, particularly in high yield securities, leveraged loans, high yield credit derivatives and distressed securities, as well as experience in operations,

6

corporate finance and mergers and acquisitions. The members of the Investment Committee have diverse backgrounds with investing experience through multiple business and credit cycles. Moreover, certain members of the Investment Committee and other executives and employees of the Adviser and its affiliates have operating and/or investing experience on behalf of business development companies. We believe this experience provides the Adviser with an in-depth understanding of the strategic, financial and operational challenges and opportunities of middle market companies and will afford it numerous tools to manage risk while preserving the opportunity for attractive risk-adjusted returns on our investments.

Distinctive Origination Platform. To date, a substantial majority of our investments have been sourced directly. We believe that our origination platform provides us the ability to originate investments without the assistance of investment banks or other traditional Wall Street intermediaries. The Investment Team includes over 50 investment professionals and is responsible for originating, underwriting, executing and managing the assets of our direct lending transactions and for sourcing and executing opportunities directly. The Investment Team has significant experience as transaction originators and building and maintaining strong relationships with private equity sponsors and companies.

The Investment Team also maintains direct contact with banks, corporate advisory firms, industry consultants, attorneys, investment banks, “club” investors and other potential sources of lending opportunities. We believe the Adviser’s ability to source through multiple channels allows us to generate investment opportunities that have more attractive risk-adjusted return characteristics than by relying solely on origination flow from investment banks or other intermediaries and to be more selective investors.

Since its inception through December 31, 2020, the Adviser and its affiliates have reviewed over 5,200 opportunities and sourced potential investment opportunities from over 530 private equity sponsors and venture capital firms. We believe that the Adviser receives “early looks” and “last looks” based on its relationships, allowing it to be highly selective in the transactions it pursues.

Potential Long-Term Investment Horizon. We believe our potential long-term investment horizon gives us flexibility, allowing us to maximize returns on our investments. We invest using a long-term focus, which we believe provides us with the opportunity to increase total returns on invested capital, as compared to other private company investment vehicles or investment vehicles with daily liquidity requirements (e.g., open-ended mutual funds and ETFs).

Defensive, Income-Orientated Investment Philosophy. The Adviser employs a defensive investment approach focused on long-term credit performance and principal protection. This investment approach involves a multi-stage selection process for each investment opportunity as well as ongoing monitoring of each investment made, with particular emphasis on early detection of credit deterioration. This strategy is designed to minimize potential losses and achieve attractive risk adjusted returns.

Active Portfolio Monitoring. The Adviser closely monitors the investments in our portfolio and takes a proactive approach to identifying and addressing sector- or company-specific risks. The Adviser receives and reviews detailed financial information from portfolio companies no less than quarterly and seeks to maintain regular dialogue with portfolio company management teams regarding current and forecasted performance. In addition, the Adviser has built out its portfolio management team to include workout experts who closely monitor our portfolio companies and assess each portfolio company’s operational and liquidity exposure and outlook. Although we may invest in “covenant-lite” loans, which generally do not have a complete set of financial maintenance covenants, we anticipate that many of our investments will have financial covenants that we believe will provide an early warning of potential problems facing our borrowers, allowing lenders, including us, to identify and carefully manage risk. Further, we anticipate that many of our equity investments will provide us the opportunity to nominate a member or observer to the board of directors of the portfolio company, which we believe will allow us to closely monitor the performance of our portfolio companies.

Investment Selection

The Adviser has identified the following investment criteria and guidelines that it believes are important in evaluating prospective portfolio companies. However, not all of these criteria and guidelines will be met, or will be equally important, in connection with each of our investments.

Established Companies with Positive Cash Flow. We seek to invest in companies with sound historical financial performance which we believe tend to be well-positioned to maintain consistent cash flow to service and repay their obligations and maintain growth in their businesses or market share in all market conditions, including in the event of a recession. The Adviser typically focuses on upper middle-market companies with a history of profitability on an operating cash flow basis. The Adviser does not intend to invest in start-up companies that have not achieved sustainable profitability and cash flow generation or companies with speculative business plans.

Strong Competitive Position in Industry. The Adviser analyzes the strengths and weaknesses of target companies relative to their competitors. The factors the Adviser considers include relative product pricing, product quality, customer loyalty, substitution risk, switching costs, patent protection, brand positioning and capitalization. We seek to invest in companies that have developed

7

leading positions within their respective markets, are well positioned to capitalize on growth opportunities and operate businesses, exhibit the potential to maintain sufficient cash flows and profitability to service their obligations in a range of economic environments or are in industries with significant barriers to entry. We seek companies that demonstrate advantages in scale, scope, customer loyalty, product pricing or product quality versus their competitors that, when compared to their competitors, may help to protect their market position and profitability.

Experienced Management Team. We seek to invest in companies that have experienced management teams. We also seek to invest in companies that have proper incentives in place, including management teams having significant equity interests to motivate management to act in concert with our interests as an investor.

Diversified Customer and Supplier Base. We generally seek to invest in companies that have a diversified customer and supplier base. Companies with a diversified customer and supplier base are generally better able to endure economic downturns, industry consolidation, changing business preferences and other factors that may negatively impact their customers, suppliers and competitors.

Exit Strategy. While certain debt investments may be repaid through operating cash flows of the borrower, we expect that the primary means by which we exit our debt investments will be through methods such as strategic acquisitions by other industry participants, an initial public offering of common stock, a recapitalization, a refinancing or another transaction in the capital markets.

Prior to making an equity investment in a prospective portfolio company, we analyze the potential for that company to increase the liquidity of its equity through a future event that would enable us to realize appreciation in the value of our equity interest. Liquidity events may include an initial public offering, a private sale of our equity interest to a third party, a merger or an acquisition of the company or a purchase of our equity position by the company or one of its stockholders.

In addition, in connection with our investing activities, we may make commitments with respect to an investment in a potential portfolio company substantially in excess of our final investment. In such situations, while we may initially agree to fund up to a certain dollar amount of an investment, we may sell a portion of such amount, such that we are left with a smaller investment than what was reflected in our original commitment.

Financial Sponsorship. We seek to participate in transactions sponsored by what we believe to be high-quality private equity and venture capital firms. We believe that a financial sponsor’s willingness to invest significant sums of equity capital into a company is an explicit endorsement of the quality of their investment. Further, financial sponsors of portfolio companies with significant investments at risk have the ability and a strong incentive to contribute additional capital in difficult economic times should operational issues arise.

Investments in Different Portfolio Companies and Industries. We seek to invest broadly among portfolio companies and industries, thereby potentially reducing the risk of any one company or industry having a disproportionate impact on the value of our portfolio; however, there can be no assurances in this regard. We seek to invest not more than 20% of our portfolio in any single industry classification and target portfolio companies that comprise 1-2% of our portfolio (with no individual portfolio company generally expected to comprise greater than 5% of our portfolio).

Investment Process Overview

Origination and Sourcing. The Investment Team has an extensive network from which to source deal flow and referrals. Specifically, the Adviser sources portfolio investments from a variety of different investment sources, including among others, private equity sponsors, management teams, financial intermediaries and advisers, investment bankers, family offices, accounting firms and law firms. The Adviser believes that its experience across different industries and transaction types makes the Adviser particularly qualified to source, analyze and execute investment opportunities with a focus on downside protection and a return of principal.

Due Diligence Process. The process through which an investment decision is made involves extensive research into the company, its industry, its growth prospects and its ability to withstand adverse conditions. If one or more members of the Investment Team responsible for the transaction determines that an investment opportunity should be pursued, the Adviser will engage in an intensive due diligence process. Though each transaction may involve a somewhat different approach, the Adviser’s diligence of each opportunity could include:

|

|

• |

understanding the purpose of the loan, the key personnel, the sources and uses of the proceeds; |

|

|

• |

meeting the company’s management and key personnel, including top level executives, to get an insider’s view of the business, and to probe for potential weaknesses in business prospects; |

|

|

• |

checking management’s backgrounds and references; |

8

|

|

|

|

• |

performing a detailed review of historical financial performance, including performance through various economic cycles, and the quality of earnings; |

|

|

• |

contacting customers and vendors to assess both business prospects and standard practices; |

|

|

• |

conducting a competitive analysis, and comparing the company to its main competitors on an operating, financial, market share and valuation basis; |

|

|

• |

researching the industry for historic growth trends and future prospects as well as to identify future exit alternatives; |

|

|

• |

assessing asset value and the ability of physical infrastructure and information systems to handle anticipated growth; |

|

|

• |

leveraging the Adviser’s internal resources and network with institutional knowledge of the company’s business; |

|

|

• |

assessing business valuation and corresponding recovery analysis; |

|

|

• |

developing downside financial projections and liquidation analysis; |

|

|

• |

reviewing environmental, social and governance (“ESG”) considerations including consulting the Sustainability Accounting Standards Board’s Engagement Guide for ESG considerations; and |

|

|

• |

investigating legal and regulatory risks and financial and accounting systems and practices. |

Selective Investment Process. After an investment has been identified and preliminary diligence has been completed, an investment committee memorandum is prepared. This report is reviewed by the members of the Investment Team in charge of the potential investment. If these members of the Investment Team are in favor of the potential investment, then a more extensive due diligence process is employed. Additional due diligence with respect to any investment may be conducted on our behalf by attorneys, independent accountants, and other third-party consultants and research firms prior to the closing of the investment, as appropriate on a case-by-case basis.

Structuring and Execution. Approval of an investment requires the unanimous approval of the Investment Committee. Once the Investment Committee has determined that a prospective portfolio company is suitable for investment, the Adviser works with the management team of that company and its other capital providers, including senior, junior and equity capital providers, if any, to finalize the structure and terms of the investment.

Inclusion of Covenants. Covenants are contractual restrictions that lenders place on companies to limit the corporate actions a company may pursue. Generally, the loans in which we expect to invest will have financial maintenance covenants, which are used to proactively address materially adverse changes in a portfolio company’s financial performance. However, to a lesser extent, we may invest in “covenant-lite” loans. We use the term “covenant-lite” to refer generally to loans that do not have a complete set of financial maintenance covenants. Generally, “covenant-lite” loans provide borrower companies more freedom to negatively impact lenders because their covenants are incurrence-based, which means they are only tested and can only be breached following an affirmative action of the borrower, rather than by a deterioration in the borrower’s financial condition. Accordingly, to the extent we invest in “covenant-lite” loans, we may have fewer rights against a borrower and may have a greater risk of loss on such investments as compared to investments in or exposure to loans with financial maintenance covenants.

Portfolio Monitoring. The Adviser monitors our portfolio companies on an ongoing basis. The Adviser monitors the financial trends of each portfolio company to determine if it is meeting its business plans and to assess the appropriate course of action with respect to our investment in each portfolio company. The Adviser has a number of methods of evaluating and monitoring the performance and fair value of our investments, which may include the following:

|

|

• |

assessment of success of the portfolio company in adhering to its business plan and compliance with covenants; |

|

|

• |

periodic and regular contact with portfolio company management and, if appropriate, the financial or strategic sponsor, to discuss financial position, requirements and accomplishments; |

|

|

• |

comparisons to other companies in the portfolio company’s industry; |

|

|

• |

attendance at, and participation in, board meetings; and |

|

|

• |

review of periodic financial statements and financial projections for portfolio companies. |

9

|

|

Structure of Investments

Our investment objective is to generate current income and, to a lesser extent, capital appreciation by targeting investment opportunities with favorable risk-adjusted returns.

We expect that generally our portfolio composition will be majority debt or income producing securities, which may include “covenant-lite” loans, with a lesser allocation to equity or equity-linked opportunities. In addition, we may invest a portion of our portfolio in opportunistic investments, which will not be our primary focus, but will be intended to enhance returns to our shareholders. These investments may include high-yield bonds and broadly-syndicated loans. Our portfolio composition may fluctuate from time to time based on market conditions and interest rates.

Covenants are contractual restrictions that lenders place on companies to limit the corporate actions a company may pursue. Generally, the loans in which we expect to invest will have financial maintenance covenants, which are used to proactively address materially adverse changes in a portfolio company’s financial performance. However, to a lesser extent, we may invest in “covenant-lite” loans. See “Investment Process Overview – Inclusion of Covenants.”

Debt Investments. The terms of our debt investments are tailored to the facts and circumstances of each transaction. The Adviser negotiates the structure of each investment to protect our rights and manage our risk. We intend to invest in the following types of debt:

|

|

• |

First-lien debt. First-lien debt typically is senior on a lien basis to other liabilities in the issuer’s capital structure and has the benefit of a first-priority security interest in assets of the issuer. The security interest ranks above the security interest of any second-lien lenders in those assets. Our first-lien debt may include stand-alone first-lien loans, “unitranche” loans (including “last out” portions of such loans), and secured corporate bonds with similar features to these categories of first-lien loans. As of December 31, 2020, 37% of our first lien debt was comprised of unitranche loans. |

|

|

• |

Stand-alone first lien loans. Stand-alone first-lien loans are traditional first-lien loans. All lenders in the facility have equal rights to the collateral that is subject to the first-priority security interest. |

|

|

• |

Unitranche loans. Unitranche loans (including “last out” portion of such loans) combine features of first-lien, second-lien and mezzanine debt, generally in a first-lien position. In many cases, we may provide the issuer most, if not all, of the capital structure above their equity. The primary advantages to the issuer are the ability to negotiate the entire debt financing with one lender and the elimination of intercreditor issues. “Last out” first-lien loans have a secondary priority behind super-senior “first out” first-lien loans in the collateral securing the loans in certain circumstances. The arrangements for a “last out” first-lien loan are set forth in an “agreement among lenders,” which provides lenders with “first out” and “last out” payment streams based on a single lien on the collateral. Since the “first out” lenders generally have priority over the “last out” lenders for receiving payment under certain specified events of default, or upon the occurrence of other triggering events under intercreditor agreements or agreements among lenders, the “last out” lenders bear a greater risk and, in exchange, receive a higher effective interest rate, through arrangements among the lenders, than the “first out” lenders or lenders in stand-alone first-lien loans. Agreements among lenders also typically provide greater voting rights to the “last out” lenders than the intercreditor agreements to which second-lien lenders often are subject. Among the types of first-lien debt in which we may invest, “last out” first-lien loans generally have higher effective interest rates than other types of first-lien loans, since “last out” first-lien loans rank below standalone first-lien loans. |

|

|

• |

Second-lien debt. Our second-lien debt may include secured loans, and, to a lesser extent, secured corporate bonds, with a secondary priority behind first-lien debt. Second-lien debt typically is senior on a lien basis to unsecured liabilities in the issuer’s capital structure and has the benefit of a security interest over assets of the issuer, though ranking junior to first-lien debt secured by those assets. First-lien lenders and second-lien lenders typically have separate liens on the collateral, and an intercreditor agreement provides the first-lien lenders with priority over the second-lien lenders’ liens on the collateral. |

|

|

• |

Mezzanine debt. Structurally, mezzanine debt usually ranks subordinate in priority of payment to first-lien and second-lien debt, is often unsecured, and may not have the benefit of financial covenants common in first-lien and second-lien debt. However, mezzanine debt ranks senior to common and preferred equity in an issuer’s capital structure. Mezzanine debt investments generally offer lenders fixed returns in the form of interest payments, which could be paid-in-kind, and may provide lenders an opportunity to participate in the capital appreciation, if any, of an issuer through an equity interest. This equity interest typically takes the form of an equity co-investment or warrants. Due to its higher risk profile and often less restrictive covenants compared to senior secured loans, mezzanine debt generally bears a higher stated interest rate than first-lien and second-lien debt. |

10

Our debt investments are typically structured with the maximum seniority and collateral that we can reasonably obtain while seeking to achieve our total return target. The Adviser seeks to limit the downside potential of our investments by:

|

|

• |

requiring a total return on our investments (including both interest and potential equity appreciation) that compensates us for credit risk; |

|

|

• |

negotiating covenants in connection with our investments consistent with preservation of our capital. Such restrictions may include affirmative covenants (including reporting requirements), negative covenants (including financial covenants), lien protection, change of control provisions and board rights, including either observation rights or rights to a seat on the board under some circumstances; and |

|

|

• |

including debt amortization requirements, where appropriate, to require the timely repayment of principal of the loan, as well as appropriate maturity dates. |

Within our portfolio, the Adviser aims to maintain the appropriate proportion among the various types of first-lien loans, as well as second-lien debt and mezzanine debt, to allow us to achieve our target returns while maintaining our targeted amount of credit risk.

Equity Investments. Our investment in a portfolio company could be or may include an equity or equity linked interest, such as a warrant or profit participation right. In certain instances, we will make direct equity investments, although those situations are generally limited to those cases where we are also making an investment in a more senior part of the capital structure of the issuer.

Investment Portfolio

As of December 31, 2020 and 2019, we had made investments with an aggregate fair value of $10.8 billion and $8.8 billion, respectively, in 119 and 98 portfolio companies, respectively. Investments consisted of the following at December 31, 2020 and 2019:

|

|

|

December 31, 2020 |

|

|

December 31, 2019 |

|

||||||||||||||||||

|

($ in thousands) |

|

Amortized Cost |

|

|

Fair Value |

|

|

Net Unrealized Gain (Loss) |

|

|

Amortized Cost |

|

|

Fair Value |

|

|

Net Unrealized Gain (Loss) |

|

||||||

|

First-lien senior secured debt investments |

|

$ |

8,483,799 |

|

|

$ |

8,404,754 |

|

|

$ |

(79,045 |

) |

|

$ |

7,136,866 |

|

|

$ |

7,113,356 |

|

|

$ |

(23,510 |

) |

|

Second-lien senior secured debt investments |

|

|

2,035,151 |

|

|

|

2,000,471 |

|

|

|

(34,680 |

) |

|

|

1,590,439 |

|

|

|

1,584,917 |

|

|

|

(5,522 |

) |

|

Unsecured debt investments |

|

|

56,473 |

|

|

|

59,562 |

|

|

|

3,089 |

|

|

|

— |

|

|

|

— |

|

|

|

— |

|

|

Equity investments(1) |

|

|

245,458 |

|

|

|

271,739 |

|

|

|

26,281 |

|

|

|

12,663 |

|

|

|

12,875 |

|

|

|

212 |

|

|

Investment funds and vehicles(2) |

|

|

107,837 |

|

|

|

105,546 |

|

|

|

(2,291 |

) |

|

|

88,888 |

|

|

|

88,077 |

|

|

|

(811 |

) |

|

Total Investments |

|

$ |

10,928,718 |

|

|

$ |

10,842,072 |

|

|

$ |

(86,646 |

) |

|

$ |

8,828,856 |

|

|

$ |

8,799,225 |

|

|

$ |

(29,631 |

) |

________________

|

|

(1) |

Includes equity investment in Wingspire Capital Holdings LLC (“Wingspire”). See “ITEM 8. – FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA – Notes to Consolidated Financial Statements – Note 3. Agreements and Related Party Transactions” for more information regarding Wingspire Capital Holdings LLC. |

|

|

(2) |

Includes equity investment in Sebago Lake. See “ITEM 8. – FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA – Notes to Consolidated Financial Statements – Note 4. Investments” for more information regarding Sebago Lake. |

As of December 31, 2020 and 2019, we had outstanding commitments to fund unfunded investments totaling $880.6 million and $891.7 million, respectively.

11

The industry composition of investments at fair value at December 31, 2020 and 2019 was as follows:

|

|

|

December 31, 2020 |

|

|

December 31, 2019 |

|

|

||

|

Advertising and media |

|

|

1.0 |

|

% |

|

2.6 |

|

% |

|

Aerospace and defense |

|

|

2.7 |

|

|

|

3.3 |

|

|

|

Automotive |

|

|

1.6 |

|

|

|

1.7 |

|

|

|

Buildings and real estate |

|

|

5.6 |

|

|

|

6.6 |

|

|

|

Business services |

|

|

5.7 |

|

|

|

5.4 |

|

|

|

Chemicals |

|

|

2.2 |

|

|

|

2.6 |

|

|

|

Consumer products |

|

|

2.3 |

|

|

|

2.7 |

|

|

|

Containers and packaging |

|

|

2.0 |

|

|

|

2.1 |

|

|

|

Distribution |

|

|

6.3 |

|

|

|

8.6 |

|

|

|

Education |

|

|

2.6 |

|

|

|

3.5 |

|

|

|

Energy equipment and services |

|

|

0.1 |

|

|

|

0.2 |

|

|

|

Financial services (1) |

|

|

2.9 |

|

|

|

1.6 |

|

|

|

Food and beverage |

|

|

8.7 |

|

|

|

7.2 |

|

|

|

Healthcare equipment and services |

|

|

3.7 |

|

|

|

8.3 |

|

|

|

Healthcare providers and services |

|

|

5.2 |

|

|

|

— |

|

|

|

Healthcare technology |

|

|

3.6 |

|

|

|

3.4 |

|

|

|

Household products |

|

|

1.4 |

|

|

|

1.5 |

|

|

|

Human resource support services (3) |

|

|

0.0 |

|

|

|

— |

|

|

|

Infrastructure and environmental services |

|

|

1.8 |

|

|

|

2.7 |

|

|

|

Insurance |

|

|

8.9 |

|

|

|

5.7 |

|

|

|

Internet software and services |

|

|

11.1 |

|

|

|

8.1 |

|

|

|

Investment funds and vehicles (2) |

|

|

1.0 |

|

|

|

1.0 |

|

|

|

Leisure and entertainment |

|

|

2.0 |

|

|

|

2.0 |

|

|

|

Manufacturing |

|

|

5.3 |

|

|

|

2.9 |

|

|

|

Oil and gas |

|

|

1.7 |

|

|

|

2.3 |

|

|

|

Professional services |

|

|

5.6 |

|

|

|

8.1 |

|

|

|

Specialty retail |

|

|

2.1 |

|

|

|

2.7 |

|

|

|

Telecommunications |

|

|

0.5 |

|

|

|

0.5 |

|

|

|

Transportation |

|

|

2.4 |

|

|

|

2.7 |

|

|

|

Total |

|

|

100.0 |

|

% |

|

100.0 |

|

% |

________________

|

|

(1) |

Includes equity investment in Wingspire. See “ITEM 8. – FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA – Notes to Consolidated Financial Statements – Note 3. Agreements and Related Party Transactions” for more information regarding Wingspire. |

|

|

(2) |

Includes investment in Sebago Lake. See “ITEM 8. – FINANCIAL STATEMENTS AND SUPPLEMENTARY DATA – Notes to Consolidated Financial Statements – Note 4. Investments” for more information regarding Sebago Lake. |

|

|

(3) |

Rounds to less than 0.1%. |

The geographic composition of investments at fair value at December 31, 2020 and 2019 was as follows:

|

|

|

December 31, 2020 |

|

|

December 31, 2019 |

|

|

||

|

United States: |

|

|

|

|

|

|

|

|

|

|

Midwest |

|

|

18.2 |

|

% |

|

19.5 |

|

% |

|

Northeast |

|

|

16.7 |

|

|

|

18.7 |

|

|

|

South |

|

|

42.3 |

|

|

|

42.8 |

|

|

|

West |

|

|

17.2 |

|

|

|

15.3 |

|

|

|

Belgium |

|

|

0.8 |

|

|

|

1.0 |

|

|

|

Canada |

|

|

1.0 |

|

|

|

0.9 |

|

|

|

Israel |

|

|

0.4 |

|

|

|

— |

|

|

|

United Kingdom |

|

|

3.4 |

|

|

|

1.8 |

|

|

|

|

|

100.0 |

|

% |

|

100.0 |

|

% |

|

12

Sebago Lake, a Delaware limited liability company, was formed as a joint venture between us and The Regents of the University of California (“Regents”) and commenced operations on June 20, 2017. Sebago Lake’s principal purpose is to make investments, primarily in senior secured loans that are made to middle-market companies or in broadly syndicated loans. Both us and Regents (the “Members”) have a 50% economic ownership in Sebago Lake. Except under certain circumstances, contributions to Sebago Lake cannot be redeemed. Each of the Members initially agreed to contribute up to $100 million to Sebago Lake. On July 26, 2018, each of the Members increased their contribution to Sebago Lake up to an aggregate of $125 million. As of December 31, 2020, each Member has funded $107.8 million of their $125 million subscriptions. Sebago Lake is managed by the Members, each of which have equal voting rights. Investment decisions must be approved by each of the Members.

We have determined that Sebago Lake is an investment company under Accounting Standards Codification (“ASC”) 946; however, in accordance with such guidance, we will generally not consolidate our investment in a company other than a wholly owned investment company subsidiary or a controlled operating company whose business consists of providing services to the Company. Accordingly, we do not consolidate our non-controlling interest in Sebago Lake.

During the year ended December 31, 2018, we acquired one investment from Sebago Lake at fair market value. The transaction generated a realized gain of $0.1 million for Sebago Lake.

As of December 31, 2020 and 2019, Sebago Lake had total investments in senior secured debt at fair value, as determined by an independent valuation firm, of $554.7 million and $478.5 million, respectively. The following table is a summary of Sebago Lake’s portfolio as of December 31, 2020 and 2019:

|

($ in thousands) |

|

December 31, 2020 |

|

|

December 31, 2019 |

|

||

|

Total senior secured debt investments(1) |

|

$ |

563,555 |

|

|

$ |

484,439 |

|

|

Weighted average spread over LIBOR(1) |

|

|

4.45 |

% |

|

|

4.56 |

% |

|

Number of portfolio companies |

|

17 |

|

|

16 |

|

||

|

Largest funded investment to a single borrower(1) |

|

$ |

49,625 |

|

|

$ |

50,000 |

|

________________

|

|

(1) |

At par. |

See “Item 7. MANAGEMENT’S DISCUSSION AND ANALYSIS OF FINANCIAL CONDITION AND RESULTS OF OPERATIONS – Portfolio and Investment Activity – Sebago Lake LLC.”

Capital Resources and Borrowings

We anticipate generating cash in the future from the issuance of common stock and debt securities and cash flows from operations, including interest received on our debt investments.

Additionally, we are permitted, under specified conditions, to issue multiple classes of indebtedness and one class of shares senior to our common stock if our asset coverage, as defined in the 1940 Act, is at least equal to 150% immediately after each such issuance. Effective June 9, 2020, our asset coverage requirement applicable to senior securities was reduced from 200% to 150% and our current target leverage ratio is 0.90x-1.25x. As of December 31, 2020 and 2019, our asset coverage was 206% and 293%, respectively. See “Regulation as a Business Development Company – Senior Securities; Coverage Ratio” below.

Furthermore, while any indebtedness and senior securities remain outstanding, we must take provisions to prohibit any distribution to our shareholders (which may cause us to fail to distribute amounts necessary to avoid entity-level taxation under the Code), or the repurchase of such securities or shares unless we meet the applicable asset coverage ratios at the time of the distribution or repurchase. In addition, we must also comply with positive and negative covenants customary for these types of indebtedness or senior securities.

13

Our debt obligations consisted of the following as of December 31, 2020 and 2019:

|

|

|

December 31, 2020 |

|

|||||||||||||

|

|

Aggregate Principal Committed |

|

|

Outstanding Principal |

|

|

Amount Available(1) |

|

|

Net Carrying Value(2) |

|

|||||

|

Revolving Credit Facility(3)(5) |

|

$ |

1,355,000 |

|

|

$ |

252,525 |

|

|

$ |

1,075,636 |

|

|

$ |

243,143 |

|

|

SPV Asset Facility II |

|

|

350,000 |

|

|

|

100,000 |

|

|

|

250,000 |

|

|

|

95,654 |

|

|

SPV Asset Facility III |

|

|

500,000 |

|

|

|

375,000 |

|

|

|

125,000 |

|

|

|

373,238 |

|

|

SPV Asset Facility IV |

|

|

450,000 |

|

|

|

295,000 |

|

|

|

155,000 |

|

|

|

291,644 |

|

|

CLO I |

|

|

390,000 |

|

|

|

390,000 |

|

|

|

— |

|

|

|

386,708 |

|

|

CLO II |

|

|

260,000 |

|

|

|

260,000 |

|

|

|

— |

|

|

|

257,686 |

|

|

CLO III |

|

|

260,000 |

|

|

|

260,000 |

|

|

|

— |

|

|

|

257,744 |

|

|

CLO IV |

|

|

252,000 |

|

|

|

252,000 |

|

|

|

— |

|

|

|

247,745 |

|

|

CLO V |

|

|

196,000 |

|

|

|

196,000 |

|

|

|

— |

|

|

|

194,128 |

|